We use necessary cookies to make our site work (for example, to manage your session). We’d also like to use some non-essential cookies (including third-party cookies) to help us improve the site. By clicking ‘Accept recommended settings’ on this banner, you accept our use of optional cookies.

Necessary cookies

Analytics cookies

Yes

Yes

Yes

No

Necessary cookies

Necessary cookies enable core functionality on our website such as security, network management, and accessibility. You may disable these by changing your browser settings, but this may affect how the website functions.

Analytics cookies

We use analytics cookies so we can keep track of the number of visitors to various parts of the site and understand how our website is used. For more information on how these cookies work please see our Cookie policy.

Our tools - how we use our balance sheet to achieve our objectives

A summary of the Bank's market operations

This section of our Market Operations Guide explains how we use our balance sheet to deliver the Bank’s statutory responsibilities for monetary and financial stability. Our tools provides further details of our individual operations.

We provide a range of facilities and operations, available on published terms to eligible financial firms. These activities usually involve the creation or management of central bank money (‘reserves’).

Sterling Monetary Framework (SMF) operations in short-term sterling money markets sit at the core of our market operations. Our SMF operations provide a mechanism for market participants to borrow or deposit money at the Bank.

The Bank also conducts regular asset sale operations, via the Asset Purchase Facility, available to eligible market participants.

We also offer facilities to firms that are not eligible for access to the SMF. These include the Alternative Liquidity Facility (ALF) - a deposit facility for UK banks that do not engage in interest-bearing activity - and the Contingent NBFI Repo Facility (CNRF), which serves to expand the range of counterparties that can borrow from the Bank during times of severe gilt market dysfunction.

Please see Our tools for further information on all our market operations.

Using our balance sheet to support our mission

Our main liabilities – banknotes and reserves – are the safest and most liquid of all financial assets. Reserves are the deposits that eligible financial firms hold at the Bank of England, and represent the ultimate means of settlement for sterling transactions.

Reserves underpin nearly all other forms of money, including the deposits individuals and businesses hold at commercial banks, making them essential to the stability of the wider financial system. Our sterling market operations control the supply of reserves and play a central role in both implementing monetary policy and supporting financial stability.

As part of successive policy interventions, the Bank significantly increased the total stock of reserves, starting in 2009 via rounds of asset purchases and funding schemes, up to a peak of £978 billion in January 2022 (as shown in Chart 1). Since then, the process of reserves expansion has reversed, and we have begun to reduce the stock of reserves. This represents a gradual transition away from a supply-driven system where reserves were abundant, to a framework where the total stock of reserves is determined by market participants’ reserves demand for transactional and precautionary reasons – a new ‘steady state’. In future steady state, market participants’ demand for reserves will be below the peak level of reserves supply, but is likely to be higher than it was prior to the 2007-08 global financial crisis.footnote [1]

Chart 1 shows the evolution of reserves supply, as well as some of the key drivers of that supply, since 2006 to end-March 2025.

Chart 1: Bank of England reserves supply and backing assets (a)

Footnotes

Source: Bank of England

(a) Coloured areas summarise the Bank’s main on-balance sheet sterling facilities. The gap between the sum of those facilities and reserves primarily reflects sterling banknotes. ‘Term Funding’ includes the Term Funding Scheme and the Term Funding Scheme with additional incentives for Small and Medium-sized Enterprises but excludes the Special Liquidity Scheme and the Funding for Lending Scheme (which were held off-balance sheet). ‘Other sterling facilities’ includes most of our regular market-wide operations, including Short-Term Open Market Operations and Long-Term Repos.

Maintaining monetary stability

The Bank's balance sheet is used to implement the Monetary Policy Committee's (MPC) decisions in order to meet the Government's target of keeping inflation at 2%.

To maintain monetary stability, we need to influence monetary conditions.footnote [2] This includes, for example, the level of prices of goods and services, and the availability of credit. The MPC can do this in two main ways: 1. setting Bank Rate, and 2. the use of asset purchases, also known as 'quantitative easing' (QE).

We keep prices steady using Bank Rate

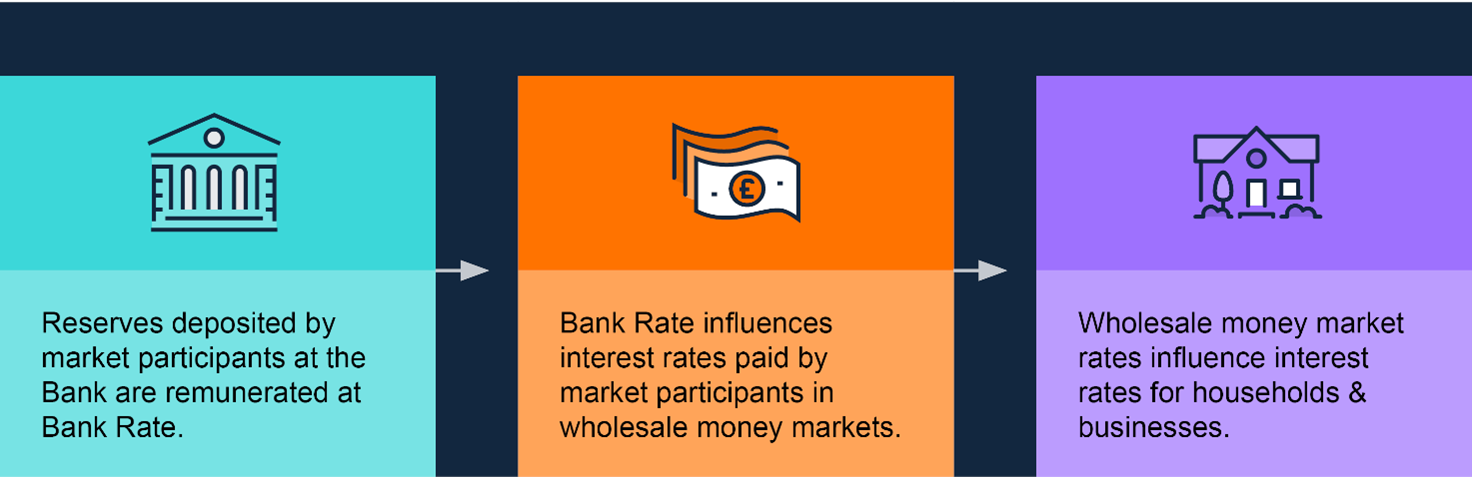

The MPC’s monetary policy stance is primarily implemented by applying interest, at Bank Rate, to reserves balances held with us by eligible financial firms. The MPC typically set Bank Rate eight times per year.

Bank Rate is the key reference rate for all other sterling interest rates. Bank Rate (and expectations about the future level of Bank Rate) influences the interest rates that financial institutions pay to borrow in wholesale money markets. This, in turn, impacts the rates paid more widely on commercial bank loans to, and deposits from, households and businesses.

To reinforce the MPC’s monetary policy stance, the interest rates we charge on our lending facilities – the Short-Term Repo (STR) and Indexed Long-Term Repo (ILTR) - are linked to Bank Rate. See Our tools for further information on our lending facilities.

Changes in longer-term interest rates can affect the price of financial assets, and changes in domestic monetary conditions can also influence the exchange rate.

Taken together, all these impacts on financial markets and associated changes in expectations impact spending decisions and inflationary pressures in the economy.

We have supported the economy using quantitative easing

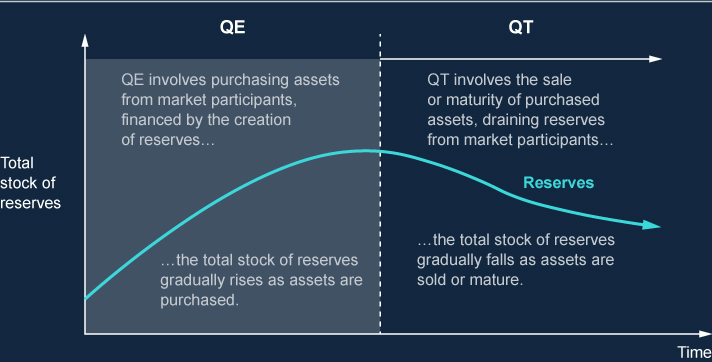

Between 2009 and 2021, the MPC used quantitative easing (QE) to help meet the inflation target. UK government debt (‘gilts’) and eligible corporate bonds were purchased from private investors in secondary markets, financed by the creation of new reserves. Those assets are held in the Asset Purchase Facility (APF).

Our stock of purchases aimed to lower the effective interest rates or ‘yields’ on the assets held. This incentivises a re-balancing of investors’ funds into other types of riskier assets, in turn pushing down on the interest rates offered on loans (since rates on government bonds tend to influence other interest rates in the economy). By holding these assets, we aimed to make it cheaper for households and businesses to borrow money, encouraging spending.

Unwinding QE

Assets purchased via QE can be unwound, this is referred to as ‘quantitative tightening’ (QT).

In February 2022, the MPC voted to begin unwinding the APF by ceasing the reinvestment of maturing gilts and corporate bonds. In September 2022, the MPC voted to begin active sales of asset holdings, and have continued to vote on the annual target for APF unwind thereafter.

Bank Rate remains the active tool when adjusting the stance of monetary policy;

Sales will be conducted so as not to disrupt the functioning of financial markets;

Sales will be conducted in a relatively gradual and predictable manner over a period of time.

As sales and maturities take place, we remove the reserves that were originally created to purchase the assets from the financial system, reducing the overall size of the Bank’s balance sheet (as shown in Chart 1).

When interest rates are low, it can be difficult for some banks and building societies to reduce deposit rates much further, limiting their ability to cut their lending rates. When Bank Rate has been low, the Bank has offered various term funding schemes to minimise these pressures and maximise the effectiveness of monetary policy pass through.

In March 2020, the Bank launched the Term Funding Scheme with additional incentives for Small- and Medium-sized Enterprises (TFSME). The TFSME was designed to help with the pass through of reductions in Bank Rate to the real economy by offering four-year funding with interest rates at, or very close to, Bank Rate. Having made £193 billion in loans, the drawdown period ended in October 2021, and the scheme is currently winding down, with most drawings maturing in 2025. Loan repayments also contribute to the reduction in the overall stock of reserves, and the overall size of the Bank’s balance sheet.

Read more about TFSME and Historic Facilities and Schemes on the Our tools page.

Anchoring interest rates to Bank Rate

The ‘supply-driven’ system

Since QE began in March 2009, the aggregate level of reserves in the economy has been largely determined by the quantity of asset purchases made by the Bank, rather than the amount eligible firms would otherwise choose to deposit in reserves accounts to manage their day-to-day liquidity needs.

This environment of abundant reserves supply has meant that firms have had little need to bid money market rates above Bank Rate to obtain reserves. At the same time, remuneration of reserves at Bank Rate means that firms have no incentive to lend excess reserves at rates below Bank Rate. Taken together, this ‘supply-driven floor system’ has kept short-term interest rates very close to Bank Rate (as illustrated on the right-hand side of Chart 2). On average, overnight wholesale interest rates have been closer to Bank Rate in the years since the system’s introduction than at any point in the preceding 20 years.

Chart 2: Monetary control under an ample supply and demand-driven system

Transitioning to a ‘demand-driven’ system

A reduction in the total stock of reserves has implications for the operation of the floor system.

Since February 2022, we have been unwinding the stock of assets purchased during QE – a process known as ‘quantitative tightening’ (QT). While QE increased the quantity of reserves, QT has the reverse effect, reducing the stock of reserves over time.

While reserves remain abundant, the MPC’s policy goals continue to be met via the supply-driven floor system. However, eventually, the supply of reserves could approach the minimum level required by firms to meet their payment obligations and broader liquidity needs – the Preferred Minimum Range of Reserves (PMRR).

At that point, firms could respond by seeking to borrow reserves in money markets, increasing the rates they are willing to pay to do so, thereby causing short-term interest rates to rise relative to Bank Rate (as illustrated on the left-hand side of Chart 2). This risks impairing the transmission of monetary policy to the wider economy.

Market participants’ overall demand for reserves is uncertain and evolves over time. Therefore, as we move closer to the PMRR, the supply-driven system will gradually become ‘demand-driven’, in which firms determine the total stock of reserves via their own transactional and precautionary demand.

SMF participants will be able to meet their demand for reserves through the use of our repo lending facilities: the STR and the ILTR. Chart 3 illustrates this transition from asset purchases being the primary source of reserves, to our repo lending facilities playing an increasingly significant role in supplying reserves to the market.

The STR was launched in 2022 to respond to fluctuations in demand for liquidity and so maintain market interest rate control as reserves fall. However, the Bank judges that the STR on its own would be insufficient to meet expected levels of system-wide reserves demand. The ILTR is expected to play an increasingly central role in supplying the stock of reserves to firms over the course of the transition.

We intend that the STR and ILTR should be used freely to access reserves as part of firms’ routine sterling liquidity management. Reflective of these facilities’ expanded role relative to the past, the PRA have confirmed this via published statements on STR and ILTR.

Further detail on the STR and ILTR facilities is included on the Our tools page.

Chart 3: Stylised Bank of England balance sheet during the APF unwind

Maintaining financial stability

Our economy is only healthy if the public has confidence in the institutions, markets and infrastructure making up the UK financial system. The Bank works to maintain financial stability by protecting and enhancing the resilience of the system as a whole.

As the ultimate means of settlement for transactions in the economy, reserves are essential to the stability of the financial system. UK banks and other financial market participants are therefore required by supervisors to hold sufficient reserves, or ‘liquidity’, to meet both transactional and precautionary needs.

The PRA sets out the size and quality of buffers that regulated firms should build up to deliver a prudent level of self-insurance against a range of stressed outflows. Further information on our liquidity rules can be found on the Capital Requirements Directive page.

However, our market operations are ‘open for business’ to complement the buffers firms maintain on their own balance sheets.

We offer lending facilities

We operate lending facilities that allow eligible firms to borrow cash (in the form of reserves), or to swap illiquid assets for more liquid ones (a collateral ‘upgrade’) at a higher cost. These include our market-wide, regular operations: the STR (against Level A collateral) and the ILTR (against the full range of eligible collateral).

As with all SMF facilities, the STR and ILTR are ‘open for business’, and intended to be used freely by firms to meet their reserves demand. This has been confirmed by PRA statements on STR and ILTR.

We also offer regular non-sterling currency operations – currently the weekly US Dollar Repo facility.

Our regular, market-wide facilities are supplemented by on-demand, bilateral facilities: Operational Standing Facilities (OSFs) and the Discount Window Facility (DWF).

Should the need arise, we can also supplement our standing lending facilities with contingent facilities: the Contingent Term Repo Facility (CTRF) and the Contingent NBFI Repo Facility (CNRF). The CNRF serves to expand the range of counterparties that can borrow from the Bank during times of severe gilt market dysfunction.

We offer lending to eligible firms which meet our prudential requirements on an ‘open for business’ basis. This means that firms know they will have access to a reliable source of liquidity at a predictable price.

Further information on all of our facilities is available in Our tools.

We convene markets to help ensure they function efficiently

We take an active interest in the effectiveness of financial markets. Markets are more likely to be efficient and effective if they are competitive, so we only allow firms access to our services if they act in a way that supports competitive and fair sterling markets.

An effective way for firms to demonstrate commitment to this is to sign the UK Money Markets Code. We endorse the Code and commit to its standards and principles. We strongly encourage all participants engaging with our market operations to do the same. Read more about our work on fair and effective markets.

We also provide a separate deposit facility on a non-interest-bearing basis

We recognise that some UK banks have formal restrictions on engaging in interest-bearing activity, leaving them with less flexibility in managing their liquidity. For these firms, we operate the Alternative Liquidity Facility (ALF), which enables them to hold a reserves-like asset using a segregated, non-interest-based model.

How a demand-driven operating framework meets our objectives

The demand-driven, repo-led frameworkfootnote [3] supports monetary control and provides an appropriate level of reserves for financial stability purposes, while retaining flexibility for the potential expansion of the Bank’s balance sheet in stress. This framework also exposes the Bank’s balance sheet to less financial risk, in contrast to supplying reserves primarily through asset purchases.

As reserves continue to decline, the Bank is working with market participants to monitor how this new framework, and the calibration of our market operations, performs against our objectives. In December 2024, the Bank published a discussion paper seeking feedback on the Bank’s transition to the new framework. In June 2025, we published a feedback statement, summarising the responses received, and outlining the Bank’s position on key issues raised.

Our facilities are ‘open for business’

All of the Bank’s market operations support our mission, and are designed to be used by firms: We are open for business.

‘Open for business’ means that participant firms which meet regulatory threshold conditions for authorisation and, for borrowing facilities, have the appropriate type and amount of collateral, have the flexibility to use our facilities as and when they deem appropriate.

In managing their liquidity, it is for firms to decide how to balance their use of market sources of funding, existing liquidity buffers, and the Bank’s facilities, depending on their business needs and the availability and cost of the different options.

Eligible firms do not have to justify their decision to use Bank facilities to the Bank or the PRA. There is no specific or limited list of cases in which firms may use our facilities, and there is no presumptive order in which we expect firms to use one form of liquidity over another.